Kingsmill Owner ABF Wins the Hovis Bread Merger: How the 'Failing Firm' Argument Cleared a Deal Regulators Usually Block

The UK's competition watchdog has cleared Associated British Foods to buy Hovis, handing the Kingsmill owner about a quarter of the bread market. The clearance rests on a rare 'failing firm' argument that shows how regulators may treat consolidation across shrinking food categories.

The Hemp-Derived THC Beverage Category 2026

A $1.1bn US category facing a binary legislative moment. Four-method sizing, the Section 781 scenario tree and the indicators that decide the category's future by November 12, 2026.

Access the report

China Private-Label Water Opportunity 2026

China's next water winners will control channels, not just brands. Private label, channel control and the margin reset — the executive intelligence read for operators, investors and CPG strategy teams sizing the China opportunity.

Access the reportA competition regulator just cleared a deal that hands one company about a quarter of the UK bread market. The reason is the surprising part. The watchdog decided that blocking the deal would not protect shoppers, because one of Britain's biggest bakers was already heading for the exit.

On 16 June 2026, the UK's Competition and Markets Authority (the CMA, Britain's competition watchdog) cleared Associated British Foods, known as ABF, to buy Hovis. ABF already owns Kingsmill. Putting Hovis and Kingsmill under one roof would normally set off alarm bells. The regulator said yes anyway, after a deep six-month investigation.

The deal nobody expected to clear

ABF agreed to buy Hovis in August 2025 from Endless, a private equity firm. The plan was to combine Hovis with ABF's own bakery arm, Allied Bakeries, which makes Kingsmill, Allinson's and Sunblest. On paper, the merger looked like the kind of deal regulators love to block. Two of the three big wrapped-bread brands in the country would answer to the same owner.

The CMA took it seriously. It skipped the usual first stage and sent the deal straight to an in-depth phase 2 review, the level reserved for the trickiest cases. Then it cleared the deal with no conditions at all.

Bread is a brutal business now

To understand the decision, look at the state of the category. Bread is one of the hardest businesses in British grocery right now. People are eating less of it. Shoppers who do buy bread increasingly reach for cheaper supermarket own-label loaves, which earn the makers very little. At the same time, the cost of wheat, energy and delivery has jumped.

The numbers show the damage. Kingsmill sales fell from £107.6 million to £73.7 million in a single year, a drop of nearly a third, pushing the brand down to fourth place. Hovis slid 8.8% to £341.1 million. Only Warburtons, the market leader, held firm, with record sales of £598.3 million. Allied Bakeries has lost money for 14 straight years.

The argument that almost never works

ABF won clearance on a legal argument that hardly ever succeeds: the failing firm defence. The idea is simple. If a business is going to leave the market anyway, then a rival buying it does not really reduce competition, because that competitor was about to vanish on its own.

Regulators treat this claim with deep suspicion, because every buyer would love to use it. Companies rarely clear the bar. ABF did. The CMA found that if the deal were blocked, the most likely outcome was that Allied Bakeries would shut down across Great Britain and Northern Ireland. With Allied gone either way, the regulator concluded the merger took nothing away from competition.

Cyrus Mehta, who chaired the inquiry, put it plainly. He said the evidence showed Allied Bakeries would likely leave the market entirely if the deal did not proceed, so the deal did not raise competition concerns.

What ABF actually gets

The merger creates the biggest bread maker in the UK. Hovis holds roughly 18% of packaged sliced bread and Allied around 6%, so the combined business lands in the low-to-mid twenties by share, level with Warburtons. Cost matters more than share here. Joining two loss-heavy bakery networks lets ABF close gaps and cut the duplication that was bleeding both sides. This deal is a bet that scale can save a shrinking business.

What it means next

The bigger story sits above bread. The CMA has shown it will allow heavy consolidation when a category is shrinking and players are failing. That is a signal to every boardroom sitting on a tired, low-growth business: a merger that looked impossible two years ago may now clear, if the decline is real and documented.

For operators, the move is to build the evidence early. Falling demand, rising costs and a long loss record are the raw material of a failing firm case. For investors and buyers, distressed assets in mature categories like ambient grocery and packaged dairy may be easier to consolidate than the market assumes. The hardest merger argument in the book just worked on a loaf of bread, and dealmakers across food and drink were watching.

Share it with your peers

Pass this analysis to colleagues who track the food and beverage market.

Submit your food & beverage project enquiry.

We’ll review it and come back with a clear plan.

Submit your project enquiry

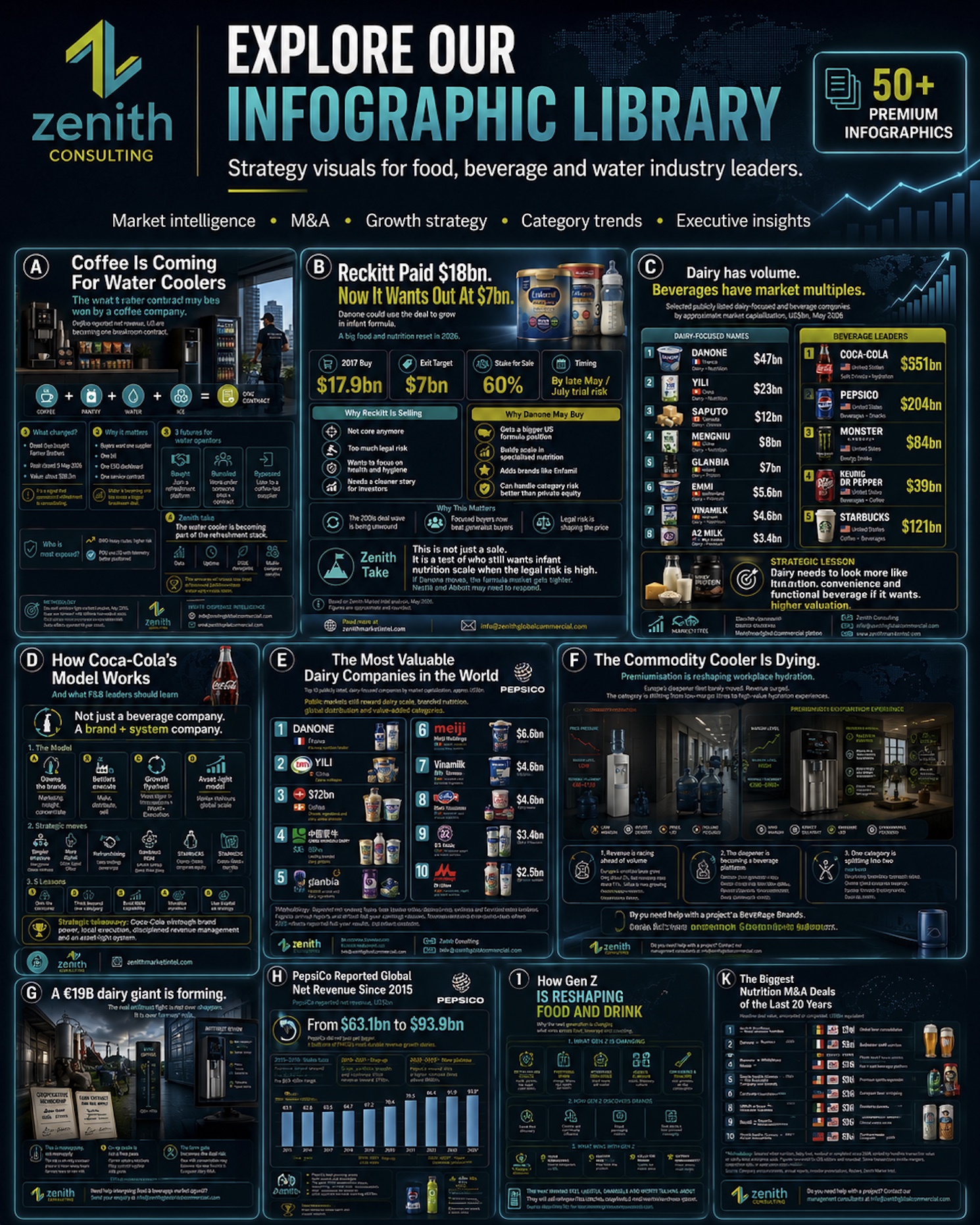

Explore our infograph library — strategy visuals for food, beverage & water leaders.

M&A deals, category growth, brand ownership, profit pools and more — at a glance. Free access for operators, investors and CPG strategy teams.

Browse the libraryStrategic Insights

📊 Analytics & Strategic Insight

How a failing-firm clearance rewrites the rules for consolidating shrinking categories

The decision most in this industry are avoiding:

👉 Hoping scale alone fixes a falling category. Scale lowers cost, but it does not bring eaters back to bread. The real prize is a slower, cheaper decline, and leaders who admit that plan better.

👉 Assuming a dominant share will always be blocked. Regulators weigh the counterfactual, meaning what happens if they say no. When the answer is a collapse, even a big combined share can clear.

👉 Treating a loss record as only a problem. A long, documented run of losses is painful, yet it is also the evidence that unlocks a merger rivals could never attempt.

Here's the full context:

→ 2010s onward: UK bread demand drifts lower as diets change and shoppers move to cheaper own-label loaves.

→ Past 14 years: ABF's Allied Bakeries, maker of Kingsmill, loses money every year despite repeated attempts to fix it.

→ August 2025: ABF agrees to buy Hovis from private equity firm Endless and combine it with Allied Bakeries.

→ Early 2026: The CMA sends the deal straight to an in-depth phase 2 review, skipping the usual first stage.

→ Most recent: On 16 June 2026 the CMA clears the deal with no conditions, after finding Allied would likely exit the market without it.

What this means for food and beverage operators and investors:

✅ The counterfactual is the whole game. In a declining category, your merger case lives or dies on what the regulator thinks happens if it says no.

✅ Distressed scale is back on the table. Deals that looked un-clearable in the growth years can pass when decline is real and the evidence is solid.

✅ Documentation is strategy. Clean records of falling demand, rising costs and multi-year losses are the raw material of a clearance, so keep them audit-ready.

3 moves you can make this week:

1️⃣ Map your declining lines. List the categories where volume and margin are both falling, and mark which could justify a failing-firm case.

2️⃣ Build the evidence file. Pull the multi-year data on demand, costs and losses that a regulator would want to see before clearing a tie-up.

3️⃣ Scan for distressed targets. Identify weak rivals in your mature categories who may welcome a buyer before they run out of road.

Take the Next Step

🧾 Go deeper on a category.

See our latest deep-dive reports, like our THC beverage report and our China market report.

→ See the latest reports

Share these strategic insights

Send the deeper analysis straight to peers who'll act on it.

Related analyses

- M&A, Investment & Valuation

Mondelez's New CFO Spent a Decade Splitting and Selling Big Food. What Amit Banati's Hire Signals for Snacking M&A

Mondelez has named Amit Banati, a CFO whose career spans the Kellogg split, Kellanova's $36 billion sale to Mars, and Kenvue's spin-off, as its new finance chief from 1 July 2026. A leadership change that looks like continuity may signal Mondelez is arming itself for snacking's next wave of deals, from a renewed Hershey approach to sharper portfolio moves.

Read analysis → - M&A, Investment & Valuation

Coca-Cola Is Selling Off Its Bottlers on Purpose: The $3.4 Billion Africa Deal Finishing a Decade-Long Asset-Light Bet

Coca-Cola has spent ten years quietly selling off its own bottling plants, and in 2026 the last big pieces are closing with a $3.4 billion Africa deal and an India sale. Here is why turning into a brand-and-recipe company reshapes its margins, and what it means for bottlers like Coca-Cola HBC and anyone buying a drinks business.

Read analysis → - M&A, Investment & Valuation

PepsiCo's 'House of Treats' and the Battle for Restaurant Drinks: Why Chains Want to Become Beverage Companies

PepsiCo has launched Pepsi 'House of Treats,' a drinks platform for restaurants and venues, to fight back as chains like Taco Bell turn drinks into a high-profit business. Here is why the next cola war will be won inside restaurants, not on the supermarket shelf.

Read analysis →

Zenith Consulting

Submit your food & beverage project enquiry.

Share your requirements. If there is a strong fit, we’ll come back with an indicative investment range, project timeline and recommended strategic approach.

Reviewed by Zenith Consulting’s senior food & beverage strategy team.

Zenith Market Intel

Need a specific food or beverage market report?

Tell us which category, region or question would be useful for your team.

Get a monthly reminder

Once a month we'll email you to check back for the latest food and beverage intelligence. No spam, just a friendly nudge.

Sister Publication

Also follow our Water Dispense Market Intelligence

Category analyses, operator briefings, and investor signals across the global water dispense market.