Big Food Is Selling Its Castoffs to Private Equity: Why Strategic Buyers Still Win 88% of Deals

Private equity is tightening its grip on food and beverage, yet strategic buyers still win about 88% of deals. The real story is that the giants are offloading the brands they no longer want, and private equity has become the preferred buyer.

The Hemp-Derived THC Beverage Category 2026

A $1.1bn US category facing a binary legislative moment. Four-method sizing, the Section 781 scenario tree and the indicators that decide the category's future by November 12, 2026.

Access the report

China Private-Label Water Opportunity 2026

China's next water winners will control channels, not just brands. Private label, channel control and the margin reset — the executive intelligence read for operators, investors and CPG strategy teams sizing the China opportunity.

Access the reportEveryone says private equity is swallowing Big Food. The numbers say something quieter. Strategic buyers, the big branded companies themselves, still drive about 88% of all food and beverage deals. Private equity is not taking over the industry. It is doing something more revealing for anyone running a brand. It is buying the products the giants have decided they no longer want, and turning other people's leftovers into a business model.

Big Food is cleaning house

The biggest theme in the industry over the past year is portfolio simplification. Large companies are selling slower-growth and non-core brands so they can pour money and management time into the categories they care about: health, nutrition, specialty ingredients and premium products. Every brand a giant decides to drop has to land somewhere, and private equity has become the preferred catcher.

The examples are stacking up fast. General Mills sold its Muir Glen organic tomato brand to Violet Foods, backed by Amphora Equity Partners. Nestlé sold Blue Bottle Coffee to Centurium Capital. In May 2026, CVC Capital Partners bought IFF's Food Ingredients business for about $4.3 billion, a textbook case of a financial buyer scooping up a non-core unit that a big company chose to shed.

Why private equity wants the leftovers

A brand that looks like an afterthought inside a $20 billion portfolio can look like a prize on its own. Private equity buys these castoffs because a standalone brand finally gets the focused attention it never had. Inside a giant, a small brand fights for shelf space, marketing budget and factory time, and usually loses. Under a dedicated owner, it gets its own team, its own targets and a clear plan to grow.

Health and wellness is where the money is heading. Consumer demand keeps shifting toward nutrition, clean labels, protein and functional benefits. In 2025, Butterfly-backed Generous Brands bought the gut-health kombucha brand Health-Ade in a deal worth around $500 million. Buyers are also chasing the ingredients behind those products. Apheon bought Cain Food Industries and merged it with Millbio to build a clean-label bakery ingredients platform.

The 88% reality

Here is the part that gets lost in the headlines. Private equity still loses most of the big fights to strategic buyers. A food and beverage M&A report from CLA Meridian Capital puts strategic acquirers at about 88% of deal activity. The reason is simple. A branded company can wring out savings that a financial buyer cannot, sharing factories, trucks and sales teams across its existing range. When a large asset comes up for sale, the strategic bidder can almost always pay more and still make the maths work.

So private equity has carved out a different lane. Its real job is portfolio transformation: buy a neglected brand, fix it, then sell it on. The exit is often a strategic buyer or a public listing a few years later. That makes many private equity owners temporary stewards rather than permanent ones, which changes how they run a brand from day one.

The headwinds slowing the buyers

The money is not as easy as it was. Borrowing costs sit well above where they were before 2022, and inflation is expected to hold near 3% in 2026. Higher rates make every leveraged deal more expensive, so buyers have grown pickier. They want stable cash flow, strong margins and a clear path to improvement before they sign. Sellers still want the rich prices of a few years ago, while buyers price in tougher conditions, and that gap drags deals out. More transactions now lean on earn-outs and retained equity to bridge the difference.

What it means for operators and investors

For operators, the lesson is to know which list you are on. If your brand is core to the parent, expect investment; if it is not, expect a sale. Working out the answer early lets a management team prepare for new ownership instead of being blindsided by it. For investors, watch the round trip. A brand sold cheaply to private equity today may return to the public market, or to a rival, in three to five years at a far higher price. The castoff you ignore now could be the competitor that takes your shelf space later.

Share it with your peers

Pass this analysis to colleagues who track the food and beverage market.

Submit your food & beverage project enquiry.

We’ll review it and come back with a clear plan.

Submit your project enquiry

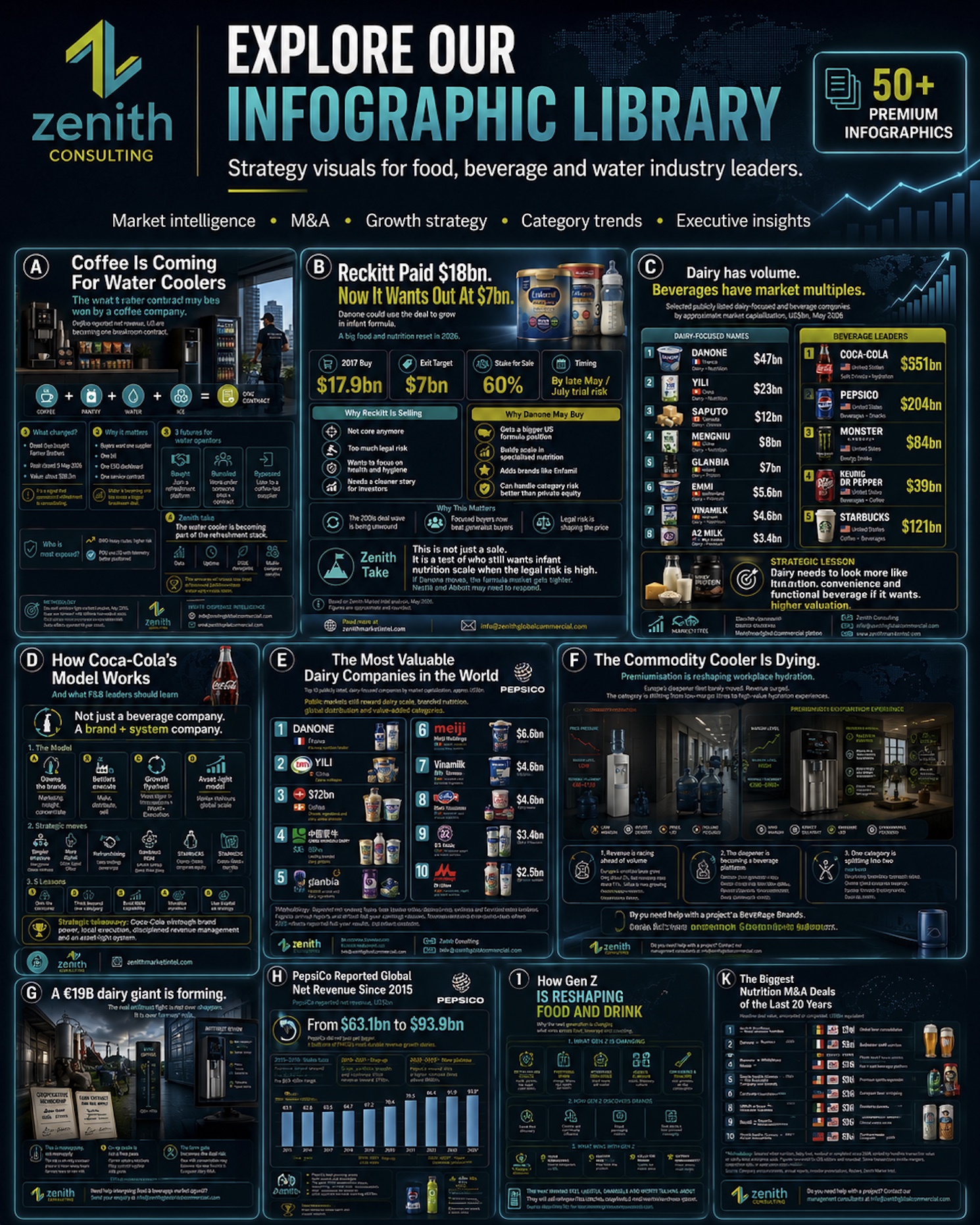

Explore our infograph library — strategy visuals for food, beverage & water leaders.

M&A deals, category growth, brand ownership, profit pools and more — at a glance. Free access for operators, investors and CPG strategy teams.

Browse the libraryStrategic Insights

📊 Analytics & Strategic Insight

Private Equity Is Not Buying Big Food. It Is Buying Big Food's Cast-Offs.

The decision most in this industry are avoiding:

👉 Treating a sale as a downgrade. A brand often grows faster under a focused owner than it ever did buried inside a giant. The "castoff" label can be a head start, not a stigma.

👉 Assuming private equity is the enemy. For a parent simplifying its portfolio, a financial buyer is the cleanest exit for a brand that needs attention the parent will never give it.

👉 Ignoring the exit clock. Private equity buys to sell. A three-to-five year exit shapes every pricing, staffing and innovation call, so read the clock before you judge the owner.

Here's the full context:

→ 2019-2024: Big Food begins a wave of portfolio simplification, shedding slower-growth and non-core brands to focus on health, nutrition and premium.

→ Jul 2025: Butterfly-backed Generous Brands buys gut-health kombucha brand Health-Ade for around $500 million, a marker of appetite for functional health brands.

→ Sep 2025: Apheon buys Cain Food Industries and merges it with Millbio to build a clean-label bakery ingredients platform.

→ May 2026: CVC Capital Partners acquires IFF's Food Ingredients business for about $4.3 billion, a textbook carve-out of a non-core unit.

→ Most recent: 26 Jun 2026 industry analysis confirms strategic buyers still drive about 88% of food and beverage deals, with private equity acting as the carve-out specialist.

What this means for food and beverage operators and investors:

✅ Carve-outs are the real pipeline. The steady flow of brands leaving big portfolios is where most private equity food deals come from, so watch closely what the giants choose to drop.

✅ Synergies still win the big auctions. A strategic buyer can pay more for scale assets, so private equity wins by buying smaller, fixing faster and selling on.

✅ Higher rates reward quality. With borrowing costly, capital flows to brands with stable cash flow and clear margin upside, not to story-led bets.

3 moves you can make this week:

1️⃣ Sort your portfolio into core and carve-out. Be honest about which brands you would invest behind and which you would sell, then act on the answer.

2️⃣ Pressure-test your brand's standalone case. If a focused owner bought it tomorrow, what would they fix first? Start doing that now, before someone else does.

3️⃣ Track the buyer of every divestiture in your category. The new owner is a forecast of who your competition will be in three years.

Take the Next Step

🧾 Go deeper on a category.

See our latest deep-dive reports, like our THC beverage report and our China market report.

→ See the latest reports

Share these strategic insights

Send the deeper analysis straight to peers who'll act on it.

Related analyses

- M&A, Investment & Valuation

Kingsmill Owner ABF Wins the Hovis Bread Merger: How the 'Failing Firm' Argument Cleared a Deal Regulators Usually Block

The UK's competition watchdog has cleared Associated British Foods to buy Hovis, handing the Kingsmill owner about a quarter of the bread market. The clearance rests on a rare 'failing firm' argument that shows how regulators may treat consolidation across shrinking food categories.

Read analysis → - M&A, Investment & Valuation

Mondelez's New CFO Spent a Decade Splitting and Selling Big Food. What Amit Banati's Hire Signals for Snacking M&A

Mondelez has named Amit Banati, a CFO whose career spans the Kellogg split, Kellanova's $36 billion sale to Mars, and Kenvue's spin-off, as its new finance chief from 1 July 2026. A leadership change that looks like continuity may signal Mondelez is arming itself for snacking's next wave of deals, from a renewed Hershey approach to sharper portfolio moves.

Read analysis → - M&A, Investment & Valuation

Coca-Cola Is Selling Off Its Bottlers on Purpose: The $3.4 Billion Africa Deal Finishing a Decade-Long Asset-Light Bet

Coca-Cola has spent ten years quietly selling off its own bottling plants, and in 2026 the last big pieces are closing with a $3.4 billion Africa deal and an India sale. Here is why turning into a brand-and-recipe company reshapes its margins, and what it means for bottlers like Coca-Cola HBC and anyone buying a drinks business.

Read analysis →

Zenith Consulting

Submit your food & beverage project enquiry.

Share your requirements. If there is a strong fit, we’ll come back with an indicative investment range, project timeline and recommended strategic approach.

Reviewed by Zenith Consulting’s senior food & beverage strategy team.

Zenith Market Intel

Need a specific food or beverage market report?

Tell us which category, region or question would be useful for your team.

Get a monthly reminder

Once a month we'll email you to check back for the latest food and beverage intelligence. No spam, just a friendly nudge.

Sister Publication

Also follow our Water Dispense Market Intelligence

Category analyses, operator briefings, and investor signals across the global water dispense market.