First General Mills, Now Hormel: Why Big Food Is Quietly Retreating From Brazil

Hormel is selling its Brazil business to a local buyer, just months after General Mills did the same. The quiet exits point to a bigger reversal: Big Food is walking back the emerging-market expansion it spent the 2010s chasing.

The Hemp-Derived THC Beverage Category 2026

A $1.1bn US category facing a binary legislative moment. Four-method sizing, the Section 781 scenario tree and the indicators that decide the category's future by November 12, 2026.

Access the report

China Private-Label Water Opportunity 2026

China's next water winners will control channels, not just brands. Private label, channel control and the margin reset — the executive intelligence read for operators, investors and CPG strategy teams sizing the China opportunity.

Access the reportIn 2017, Hormel Foods paid $104 million to buy its way into Brazil and called it a platform for growth across South America. In July 2026, it is paying its way back out.

The maker of Spam, Planters and Skippy has agreed to sell its Brazilian business, the Ceratti brand of mortadella, sausage and salami, to local producer Zanchetta Alimentos. Financial terms were not disclosed, and the deal is expected to close within weeks pending regulatory approval. For a company with roughly $12 billion in annual sales, the money involved is small. The money involved is small; the signal is not.

A quiet admission that the growth bet failed

Hormel bought Ceratti owner Cidade do Sol in 2017 to enter one of the world's largest protein markets. The logic was textbook: a rising middle class, growing meat consumption, and a base to build on. Eight years later, the base never scaled.

On the company's fourth-quarter earnings call in December 2025, interim CEO Jeffrey Ettinger was blunt. Brazil, he said, was "challenged" and had been "a drag in terms of our overall performance," hurting the international unit's ability to hit its growth targets. "Everything is under review," he added. "We do continue to look at our portfolio in total for what makes sense, what doesn't." The Ceratti sale is the first visible answer.

Brazil is turning into a Big Food exit door

Hormel is not alone, and it is not even first. In March 2026, General Mills agreed to sell its Brazilian business to local group 3corações for about $153 million (800 million reais), part of the same push to lift margins and sharpen where it competes abroad. Two American food giants have now walked out of Brazil inside four months, and both handed their assets to domestic buyers.

That last detail matters. A decade ago, the flow ran the other way. US and European majors bought into emerging markets to catch demand their home markets could no longer deliver. The buyers today are regional champions like Zanchetta and 3corações, picking up assets that global players could not make work. The globalization playbook is running in reverse.

Focus is beating footprint

The retreat is deliberate. Hormel is midway through a "Transform and Modernize" program, built by new president John Ghingo, that targets $250 million in annual savings through supply-chain fixes and a simpler portfolio. Earlier in 2026 the company sold its commodity whole-bird turkey business so Jennie-O could concentrate on higher-margin ground turkey and deli meat. Selling Brazil follows the same rule: keep what earns, exit what distracts.

The timing sharpens the point. At home, Hormel is riding strong demand for protein, with Spam and Planters gaining as shoppers trade into affordable, shelf-stable meat and snacks. This is not a company retreating from weakness across the board. It is choosing to put capital where returns are highest and pull it out of a market that soaked up management attention for a thin payoff.

It is a rule the whole sector is now following. Nestlé is cutting to four core units and offloading water and ice cream. Kraft Heinz has centralized buying rather than chase scale it cannot digest. Unilever is spinning out its ice cream arm. In a slow-growth, cost-heavy market, a tighter business that earns more beats a bigger one that earns less.

What it means for operators, investors and buyers

For operators, the lesson is that geographic reach is no longer a trophy. Every market a company holds now has to clear a return bar or become a candidate for sale. For investors, the wave of small, unglamorous divestitures is worth watching closely, because it often signals a management team getting honest about where it actually makes money. And for buyers, especially regional players and private capital, the pullback is an opening: global majors are now willing sellers of assets they once called strategic, at prices set by their urgency to simplify rather than the asset's peak value. Brazil may be the canary. The list of markets under review is longer than one country.

Share it with your peers

Pass this analysis to colleagues who track the food and beverage market.

Submit your food & beverage project enquiry.

We’ll review it and come back with a clear plan.

Submit your project enquiry

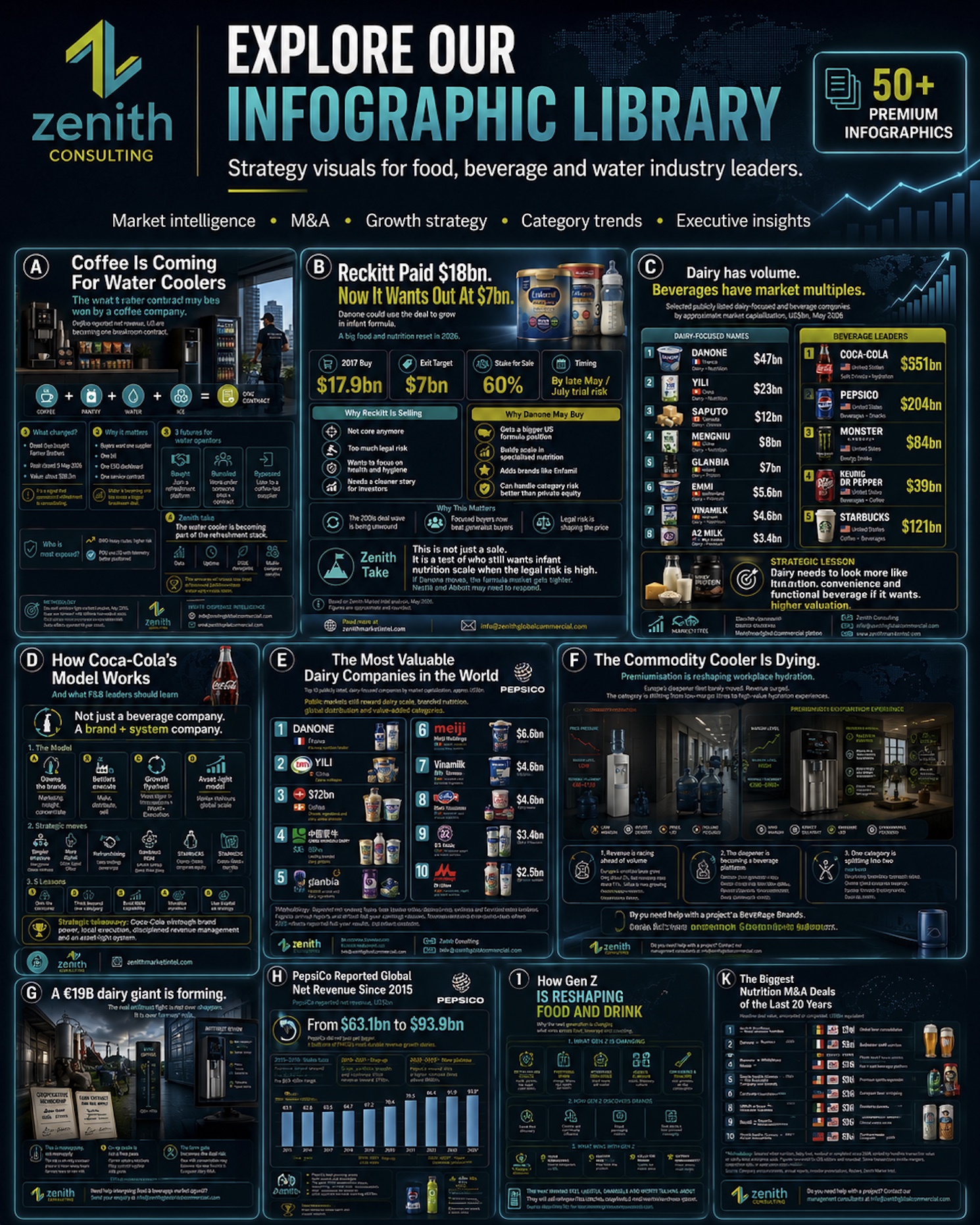

Explore our infograph library — strategy visuals for food, beverage & water leaders.

M&A deals, category growth, brand ownership, profit pools and more — at a glance. Free access for operators, investors and CPG strategy teams.

Browse the libraryStrategic Insights

📊 Analytics & Strategic Insight

The retreat from Brazil is a portfolio-discipline signal, not a Brazil story

The decision most in this industry are avoiding:

👉 Reach was never the moat. Many boards still read a map full of flags as strategic strength. The market is now paying for return on capital, not square footage, and the markets nobody can make money in are liabilities dressed as assets.

👉 The buyer tells you who really has the edge. Global majors are selling emerging-market assets to local champions like Zanchetta and 3corações. That is an admission that scale and a famous brand did not beat local cost, distribution and cultural fit.

👉 Small divestitures carry big information. A $104 million entry unwound quietly says more about management honesty than a headline megadeal does. Investors who only track the big transactions miss the tell.

Here's the full context:

→ 2010s: US and European food majors pile into Brazil and other emerging markets, chasing demand their slowing home markets could not supply.

→ 2017: Hormel pays $104 million for Cidade do Sol, owner of the Ceratti brand, to enter Brazil as a platform for South American growth.

→ December 2025: Hormel's interim CEO calls Brazil "challenged" and "a drag," and puts the entire portfolio under review.

→ March 2026: General Mills agrees to sell its Brazil business to local group 3corações for about $153 million to lift margins and refocus abroad.

→ Most recent: On 1 July 2026 Hormel agrees to sell Ceratti to Zanchetta Alimentos, the second US food giant to exit Brazil in four months.

What this means for food and beverage operators and investors:

✅ Put every market on a return clock. A country that cannot clear its cost of capital is a sale candidate, however long you have held it. A feeling about "presence" is not a strategy.

✅ Read the small print of divestitures. A cluster of quiet exits usually means a management team is getting honest about where it earns, and that honesty tends to come before better capital allocation and, often, a re-rating.

✅ Local buyers are the new counterparties. If you run a regional business, the majors are now willing sellers of assets they once called core, so pipeline those assets before the bankers do.

3 moves you can make this week:

1️⃣ Rank your markets by return, not revenue. Build a simple table of each geography's operating margin and the capital tied up in it. The bottom of that list is your divestiture shortlist.

2️⃣ Pressure-test your "platform" bets. For any market you entered to "build a platform," ask what it has actually earned since. If the platform never came, price an exit now, not after another weak year.

3️⃣ Map the willing sellers in your category. List the global players signaling simplification and the assets they are likely to shed. One of them may be your cheapest route into a market or segment you want.

Take the Next Step

💬 You don't need a written brief.

Tell us what you are weighing up, and we will come back with the likely project scope, recommended direction and cost range.

→ Tell us what you're planning

Share these strategic insights

Send the deeper analysis straight to peers who'll act on it.

Related analyses

- Corporate Strategy & Portfolio

Kraft Heinz Scrapped Its Breakup. Its New Reorg Puts One Executive Over All Buying

Five months after scrapping its planned breakup, Kraft Heinz has reorganised into three regions and handed one executive control of all procurement and supply chain. The quiet 1 July reorg is a bet that centralising a $25 billion food company beats splitting it, and suppliers should read it closely.

Read analysis → - Corporate Strategy & Portfolio

KFC Is Rolling Its Own Drinks Brand Into 3,000 Stores: The Quiet Threat to Coca-Cola and PepsiCo's Fountain Empire

KFC is rolling its own Kwench drinks brand into roughly 3,000 stores this year, backed by £38 million of UK and Ireland investment. Restaurant chains are turning into beverage companies, and that changes the away-from-home math for Coca-Cola, PepsiCo and Keurig Dr Pepper.

Read analysis → - Corporate Strategy & Portfolio

Constellation Brands Q1 FY2027: Beer Now Carries 94% of the Business as Wine Sales Halve

Constellation Brands reported wine and spirits sales down 47% in its latest quarter, yet the stock rose almost 4%. The Modelo owner has become a near-pure Mexican beer company, and that concentration is both its edge and its biggest risk.

Read analysis →

Zenith Consulting

Submit your food & beverage project enquiry.

Share your requirements. If there is a strong fit, we’ll come back with an indicative investment range, project timeline and recommended strategic approach.

Reviewed by Zenith Consulting’s senior food & beverage strategy team.

Zenith Market Intel

Need a specific food or beverage market report?

Tell us which category, region or question would be useful for your team.

Get a monthly reminder

Once a month we'll email you to check back for the latest food and beverage intelligence. No spam, just a friendly nudge.

Sister Publication

Also follow our Water Dispense Market Intelligence

Category analyses, operator briefings, and investor signals across the global water dispense market.