Kraft Heinz Scrapped Its Breakup. Its New Reorg Puts One Executive Over All Buying

Five months after scrapping its planned breakup, Kraft Heinz has reorganised into three regions and handed one executive control of all procurement and supply chain. The quiet 1 July reorg is a bet that centralising a $25 billion food company beats splitting it, and suppliers should read it closely.

The Hemp-Derived THC Beverage Category 2026

A $1.1bn US category facing a binary legislative moment. Four-method sizing, the Section 781 scenario tree and the indicators that decide the category's future by November 12, 2026.

Access the report

China Private-Label Water Opportunity 2026

China's next water winners will control channels, not just brands. Private label, channel control and the margin reset — the executive intelligence read for operators, investors and CPG strategy teams sizing the China opportunity.

Access the reportIn September 2025, Kraft Heinz told the market it would break itself into two companies. Ten months later, it has done close to the opposite. As of 1 July 2026, Kraft Heinz runs as one tighter machine, with a single executive now in charge of everything the company buys. The maker of Heinz, Philadelphia and Oscar Mayer has folded its operating regions down to three and merged procurement and supply chain into one global function. It is a quiet reorganisation, and it may matter more than the breakup ever would have.

What actually changed on 1 July

Kraft Heinz now runs on three regions instead of a wider spread of units. North America stays under Nico Amaya. Europe and Pacific Developed Markets stays under Willem Brandt. A new Emerging Markets region, led by Marcel Regis, pulls together the old Asia and West-and-East emerging market teams. The bigger move sits underneath: procurement and supply chain are now one central function under a single global chief, Janelle Aydin. Two senior leaders, the omnichannel sales and Asia emerging markets chief and the global supply chain chief, step back into advisory roles.

From two companies to one tighter machine

Rewind to September 2025. Kraft Heinz planned to split into a roughly $15 billion "Global Taste Elevation" business built on sauces and spreads, and a roughly $10 billion "North American Grocery" business holding Kraft Singles, Lunchables and Oscar Mayer. The idea was simple: two focused companies would be worth more than one sprawling one. New chief executive Steve Cahillane paused that plan in February 2026 and bet $600 million on a turnaround instead. Warren Buffett's Berkshire Hathaway, which held about 28% of the company, had argued the split would be costly and would not create real value.

When you cannot unlock value by breaking a company apart, the next lever is to take cost and slowness out of the middle. That is what this reorg does. Fewer regions means fewer layers and faster decisions. One buying function means the whole company negotiates as a single customer.

Why one buying desk matters

Kraft Heinz spends heavily on the same raw materials in every market: tomatoes, dairy, coffee, meat, sugar and packaging. Splitting those buys across regions leaves scale on the table. Pulling roughly $25 billion of sales behind one procurement and supply chain team is a real margin lever, especially with commodity costs still swinging. A central desk can standardise contracts, push volume to fewer suppliers and move faster when a crop or a currency turns. Done well, it drops straight to gross margin. Done badly, it slows the plants down and annoys the customers who liked the old local service.

What it means for suppliers and rivals

For the companies that sell to Kraft Heinz, the message is blunt. Fewer, bigger buying desks mean harder negotiations and fewer places to pitch. A supplier who once sold to three regional teams may soon face one global buyer with more leverage and better data. This mirrors what is happening on the retail side, where grocers keep merging into larger buyers. Squeezed in the middle, mid-size ingredient and packaging firms have their own reason to get bigger.

Kraft Heinz is not alone. Nestlé, Unilever and Mondelez have all been trimming layers and centralising functions to defend margins as volumes stay soft. The risk in every one of these programmes is the same: a tighter centre can react slower to local markets and lose the feel for what shoppers in each country actually want.

What to watch next

The breakup is on pause. A cleaner three-region structure with one supply chain would, oddly, make a future split easier to run if the board ever revives it. For now, the test is financial. Watch whether this shows up as better gross margin and faster decisions by 2027, or just a tidier org chart with the same soft sales. Cahillane has spent his first year telling investors the problems are fixable and within his control. This reorg is the clearest sign yet of how he plans to prove it, and Berkshire, still weighing its exit, will be reading the same scoreboard.

Share it with your peers

Pass this analysis to colleagues who track the food and beverage market.

Submit your food & beverage project enquiry.

We’ll review it and come back with a clear plan.

Submit your project enquiry

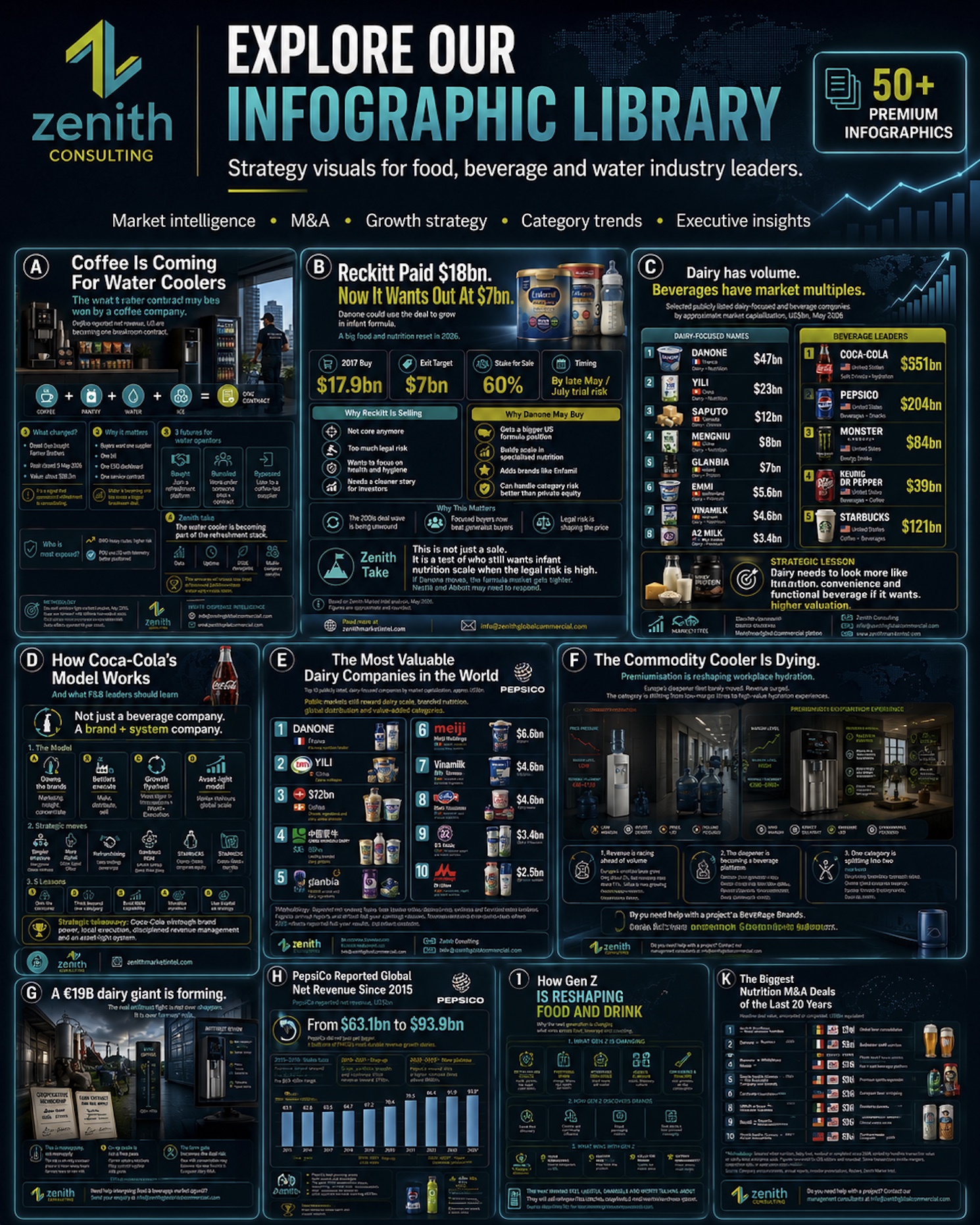

Explore our infograph library — strategy visuals for food, beverage & water leaders.

M&A deals, category growth, brand ownership, profit pools and more — at a glance. Free access for operators, investors and CPG strategy teams.

Browse the libraryStrategic Insights

📊 Analytics & Strategic Insight

Centralisation is the new breakup: when you cannot sell the parts, you squeeze the seams

The decision most in this industry are avoiding:

👉 Most boards treat a reorg as an HR event, not a margin strategy. The real prize here is procurement scale, yet few name a hard savings number for it, so the benefit stays vague and no single person owns it.

👉 A breakup and a centralisation solve the same problem from opposite ends. One narrows focus by cutting the company in half. The other widens buying power by pulling it together. Picking the wrong one can burn two years.

👉 Almost no one models the customer cost of centralising. A global buying desk saves on inputs and can quietly lose the local relationships that kept a retailer or a foodservice account loyal. That trade rarely shows up in the board deck.

Here's the full context:

→ 2015: Kraft and Heinz merge under 3G Capital and Berkshire, on a cost-cutting model built around zero-based budgeting.

→ 2023 to 2024: Years of tight spending show up as tired brands and flat volumes; the cost machine runs out of road.

→ September 2025: Kraft Heinz announces a plan to split into two public companies, a roughly $15 billion sauces and spreads business and a roughly $10 billion grocery business.

→ February 2026: New CEO Steve Cahillane pauses the split and commits $600 million to a turnaround; Berkshire, at about 28%, backs the pause.

→ Most recent: On 1 July 2026 the company reorganises into three regions and places procurement and supply chain under one global chief.

What this means for food and beverage operators and investors:

✅ Buying power is now a board-level asset. The winners will set a procurement savings target and track it like revenue, rather than bury it inside a word like "synergies."

✅ Supplier concentration cuts both ways. One global desk gets better prices and more exposure if a single supplier fails, so dual-sourcing discipline matters more, not less.

✅ A clean structure is optionality. Three tidy regions with one supply chain can be run harder, sold in pieces, or split later. The reorg buys flexibility whichever way the board turns.

3 moves you can make this week:

1️⃣ Map your own buying desks. Count how many separate teams negotiate the same inputs. Every duplicate is a discount you are leaving on the table.

2️⃣ Pressure-test a centralisation before you commit to a sale. Model the margin from combining functions against the value of splitting, and run both cases side by side.

3️⃣ Call your three biggest suppliers. If your customers are centralising, assume yours will too. Lock terms and line up a second source before the leverage shifts.

Take the Next Step

🧭 Facing a decision like this in your own category?

Describe it in a few lines. Selected enquiries receive an initial strategic assessment: direction, likely scope and indicative investment range.

→ Start a project enquiry

Share these strategic insights

Send the deeper analysis straight to peers who'll act on it.

Related analyses

- Corporate Strategy & Portfolio

KFC Is Rolling Its Own Drinks Brand Into 3,000 Stores: The Quiet Threat to Coca-Cola and PepsiCo's Fountain Empire

KFC is rolling its own Kwench drinks brand into roughly 3,000 stores this year, backed by £38 million of UK and Ireland investment. Restaurant chains are turning into beverage companies, and that changes the away-from-home math for Coca-Cola, PepsiCo and Keurig Dr Pepper.

Read analysis → - Corporate Strategy & Portfolio

Constellation Brands Q1 FY2027: Beer Now Carries 94% of the Business as Wine Sales Halve

Constellation Brands reported wine and spirits sales down 47% in its latest quarter, yet the stock rose almost 4%. The Modelo owner has become a near-pure Mexican beer company, and that concentration is both its edge and its biggest risk.

Read analysis → - Corporate Strategy & Portfolio

Beef Tallow's $1.1 Billion Comeback: Why Conagra, Utz and PepsiCo Are Rethinking the Fat in Your Snacks

Sales of food made with beef tallow hit $1.1 billion, up 275% in three years, after a federal guideline change endorsed the once-shunned fat. Conagra, Utz and PepsiCo are now rethinking the oil in the fryer, but shopper data suggests the trend is louder than it is real.

Read analysis →

Zenith Consulting

Submit your food & beverage project enquiry.

Share your requirements. If there is a strong fit, we’ll come back with an indicative investment range, project timeline and recommended strategic approach.

Reviewed by Zenith Consulting’s senior food & beverage strategy team.

Zenith Market Intel

Need a specific food or beverage market report?

Tell us which category, region or question would be useful for your team.

Get a monthly reminder

Once a month we'll email you to check back for the latest food and beverage intelligence. No spam, just a friendly nudge.

Sister Publication

Also follow our Water Dispense Market Intelligence

Category analyses, operator briefings, and investor signals across the global water dispense market.