Danone's A$2bn Australia Double Deal: Made Group, the Saputo Buyout, and Big Food's Protein and Gut-Health Land Grab

Danone has agreed two Asia-Pacific deals in a single day, buying Australia's Made Group for a reported A$2 billion and taking full control of its Saputo fresh dairy joint venture. The double swoop shows how Big Food is paying growth-stock prices to own the protein and gut-health brands it cannot build fast enough.

The Hemp-Derived THC Beverage Category 2026

A $1.1bn US category facing a binary legislative moment. Four-method sizing, the Section 781 scenario tree and the indicators that decide the category's future by November 12, 2026.

Access the report

China Private-Label Water Opportunity 2026

China's next water winners will control channels, not just brands. Private label, channel control and the margin reset — the executive intelligence read for operators, investors and CPG strategy teams sizing the China opportunity.

Access the reportDanone just agreed to pay a reported A$2 billion for an Australian drinks business that booked about €300 million in sales last year. That works out to roughly four times revenue for a maker of coconut water, protein smoothies and gut-health yoghurt.

On 22 June 2026, Danone announced two Asia-Pacific deals on the same day. It agreed to buy Made Group, a fast-growing Australian beverage company. It also moved to take full control of its Australian fresh dairy joint venture with Saputo. The message is hard to miss: Danone is buying its next phase of growth, and it is buying it in Asia.

Two deals in one day

Made Group was founded in 2005 and has built a portfolio of health-focused drinks. It owns Cocobella, the coconut water and yoghurt brand, Rokeby, a protein smoothie line, Impressed cold-pressed juices, and Nutrientwater, billed as Australia's first enhanced water. The company sells across Australia, New Zealand and Southeast Asia. Danone said Made delivered double-digit growth and strong margins, with sales topping €300 million ($344 million) for the year ending June 2026.

The reported price tells you how Danone sees it. Australia's Financial Review put the deal at about A$2 billion, though Danone did not confirm terms. At that level, Danone paid a growth-stock price for growth it could not generate fast enough on its own. Coconut water and protein shakes do not usually trade at four times sales. Functional drinks that are still compounding double digits do.

Why Danone paid up

The logic sits in two words that run through almost every Big Food deal this year: protein and gut health. Made's range plugs straight into both. High-protein ready-to-drink products and gut-friendly yoghurts are two of the fastest-moving corners of nutrition, lifted by GLP-1 weight-loss drugs that push users toward protein and lighter, functional foods. Danone is buying a ready-made answer to the question every food maker is now asking: where is the healthy growth.

It also buys a bigger footprint in a region where Danone has been thin. Made's presence across Australia, New Zealand and Southeast Asia gives Danone distribution and local brands it would take years to build from scratch. The company called Made a meaningful contributor to its Essential Dairy and Plant-based business in the Asia-Pacific.

Taking full control of the Saputo brands

The second deal is quieter but just as telling. Danone will buy the 49% of its Australian fresh dairy joint venture it does not already own from Saputo. That hands it sole ownership of YoPRO, Activia and Ultimate, the functional yoghurt brands the partnership built. Buying out Saputo gives Danone every cent of upside from its fastest-selling Australian yoghurts instead of half. For Saputo, selling the stake fits a wider tidy-up of a dairy portfolio it has been pruning for two years.

Bolt-ons under the radar

There is a regulatory lesson buried in the timing. Danone's €1 billion bid for UK meal-replacement brand Huel is stuck in a Competition and Markets Authority review, with a market consultation that closed on 10 June feeding a formal investigation. The Australian deals, by contrast, are small enough to clear quietly while the headline acquisition draws the scrutiny. Big Food is learning that a string of digestible bolt-ons can rebuild a portfolio faster than one trophy deal that regulators can freeze for a year.

What it means next

For Danone, this is chief executive Antoine de Saint-Affrique's strategy in plain view: trade slow categories for fast ones, and pay up where the growth is real. Expect more bolt-ons in protein, gut health and functional drinks, especially in Asia, where the company is under-represented and the middle class is still expanding.

For everyone else in food and beverage, the read is sharper. When a category grows faster than you can build, the cheapest entry ticket is often the one you buy. The brands compounding double digits in protein and gut health are getting bid up now, while they are still independent. Operators sitting on one of those assets have rarely had more leverage, and buyers who wait will pay even more than four times sales.

Share it with your peers

Pass this analysis to colleagues who track the food and beverage market.

Submit your food & beverage project enquiry.

We’ll review it and come back with a clear plan.

Submit your project enquiry

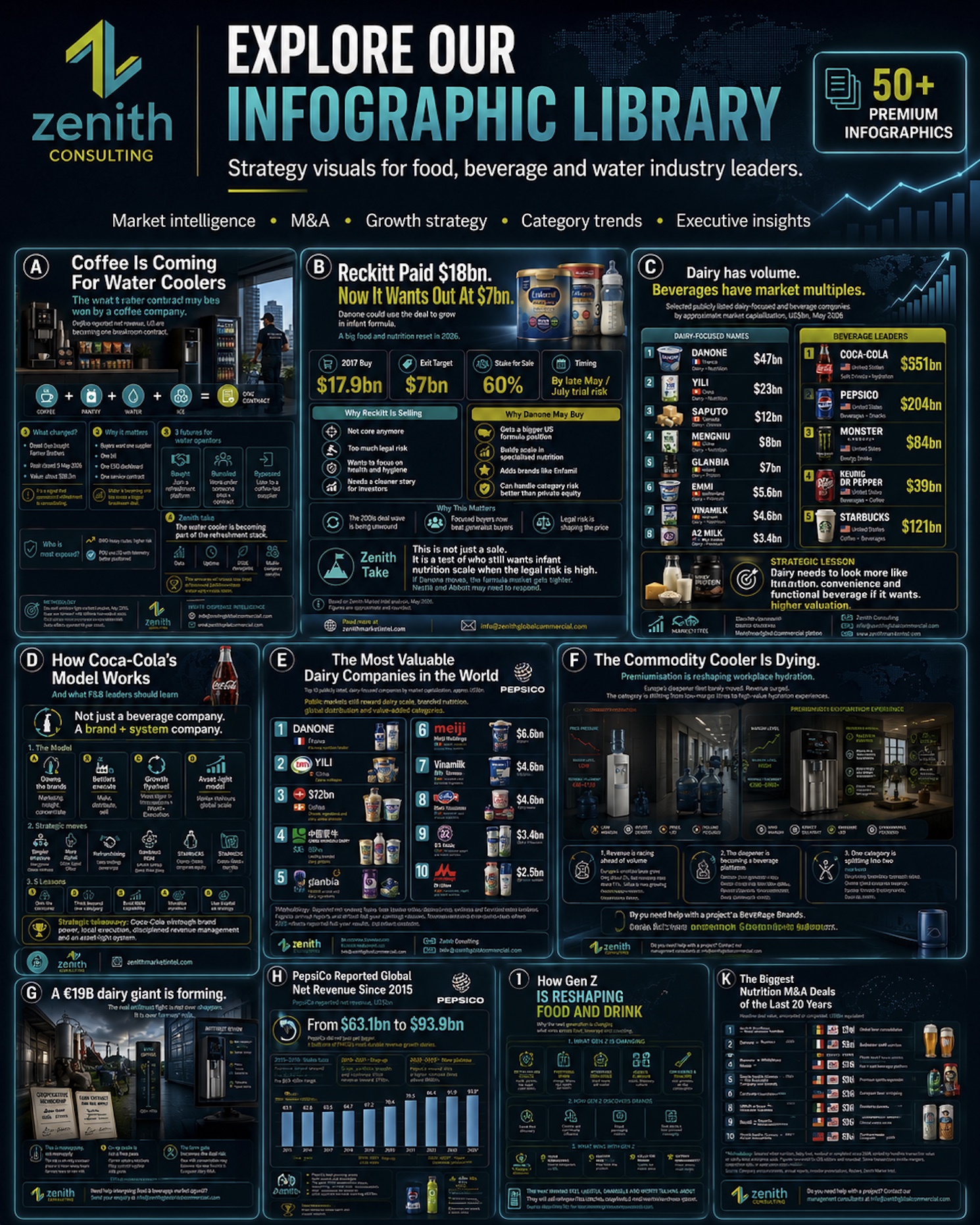

Explore our infograph library — strategy visuals for food, beverage & water leaders.

M&A deals, category growth, brand ownership, profit pools and more — at a glance. Free access for operators, investors and CPG strategy teams.

Browse the libraryStrategic Insights

📊 Analytics & Strategic Insight

Big Food is buying the protein and gut-health growth it cannot build

The decision most in this industry are avoiding:

👉 Waiting for functional brands to get cheaper. They are getting more expensive. Every quarter of double-digit growth raises the multiple a buyer has to pay.

👉 Treating Asia-Pacific as a later problem. Danone just paid up to enter now, because local brands with regional distribution are scarce and disappearing into bigger hands.

👉 Reading the Saputo buyout as housekeeping. Taking full control of a joint venture is a growth decision: you stop sharing the upside on your best-selling lines.

Here's the full context:

→ 2005: Made Group is founded in Australia and starts building health-focused drink brands led by Cocobella coconut water.

→ April 2026: Danone agrees to buy UK meal-replacement brand Huel for about €1 billion, signalling a deeper push into functional nutrition.

→ May 2026: Danone expands its Oikos ready-to-drink protein range in North America, chasing the same protein demand.

→ June 2026 (early): Danone's Huel deal enters a UK Competition and Markets Authority review after a market consultation closes on 10 June.

→ Most recent: On 22 June 2026, Danone agrees to buy Made Group for a reported A$2 billion and to take full control of its Saputo fresh dairy joint venture in Australia.

What this means for food and beverage operators and investors:

✅ Functional assets are repricing upward. A double-digit grower in protein or gut health now commands a growth multiple, so budget for it or move first.

✅ Bolt-ons beat trophy deals on speed. Smaller, regional purchases clear regulators while a single large deal can sit in review for a year.

✅ Joint ventures are worth a second look. Owning all of a winning brand captures every bit of the upside and removes a partner who may not share your ambition.

3 moves you can make this week:

1️⃣ List your functional winners. Flag every brand in your portfolio growing double digits in protein, gut health or hydration, and value it as if a buyer called tomorrow.

2️⃣ Map the independents. Build a short list of fast-growing regional brands in your category that still lack a big parent, before a rival buys them.

3️⃣ Review your joint ventures. Check which partnerships hold your best growth, and decide whether full control is worth buying out the other side.

Take the Next Step

🧭 Got a project in mind?

Send us your thoughts and project requirements and our consultants will build you a project plan.

→ Start a project enquiry

Share these strategic insights

Send the deeper analysis straight to peers who'll act on it.

Related analyses

- Health, Nutrition & Functional

Nestlé Taps Lab-Made Breast Milk Protein: How Precision Fermentation Is Rewriting the Infant Formula Moat

Nestlé has partnered with biotech startup Helaina to put precision-fermented human lactoferrin into infant formula, brewing a once-scarce breast milk protein in tanks instead of pulling it from cow's milk. The deal shows how fermentation could loosen Big Dairy's grip on the high-margin proteins behind premium baby formula.

Read analysis → - Health, Nutrition & Functional

Danone Sues Chobani Over 20-Gram Protein Claims: The Serving-Size Loophole Behind the Yogurt Protein Wars

Danone has sued Chobani in federal court, alleging its rival inflates the protein on its 20G yogurt tubs by using a bigger-than-standard serving size. The case shows how a single 20-gram claim, supercharged by GLP-1 demand, has turned label math into a competitive weapon across food and beverage.

Read analysis → - Health, Nutrition & Functional

Milkfat Is Winning the Dairy Glut: Why Butter Is Firm and Milk Powder Is Crashing for Arla, Fonterra and Lactalis

The world is making far too much milk, yet butter keeps getting more expensive while milk powder collapses. Here is why the dairy glut is splitting in two and quietly redrawing the margin map for Arla, Fonterra, Lactalis and every big dairy processor.

Read analysis →

Zenith Consulting

Submit your food & beverage project enquiry.

Share your requirements. If there is a strong fit, we’ll come back with an indicative investment range, project timeline and recommended strategic approach.

Reviewed by Zenith Consulting’s senior food & beverage strategy team.

Zenith Market Intel

Need a specific food or beverage market report?

Tell us which category, region or question would be useful for your team.

Get a monthly reminder

Once a month we'll email you to check back for the latest food and beverage intelligence. No spam, just a friendly nudge.

Sister Publication

Also follow our Water Dispense Market Intelligence

Category analyses, operator briefings, and investor signals across the global water dispense market.